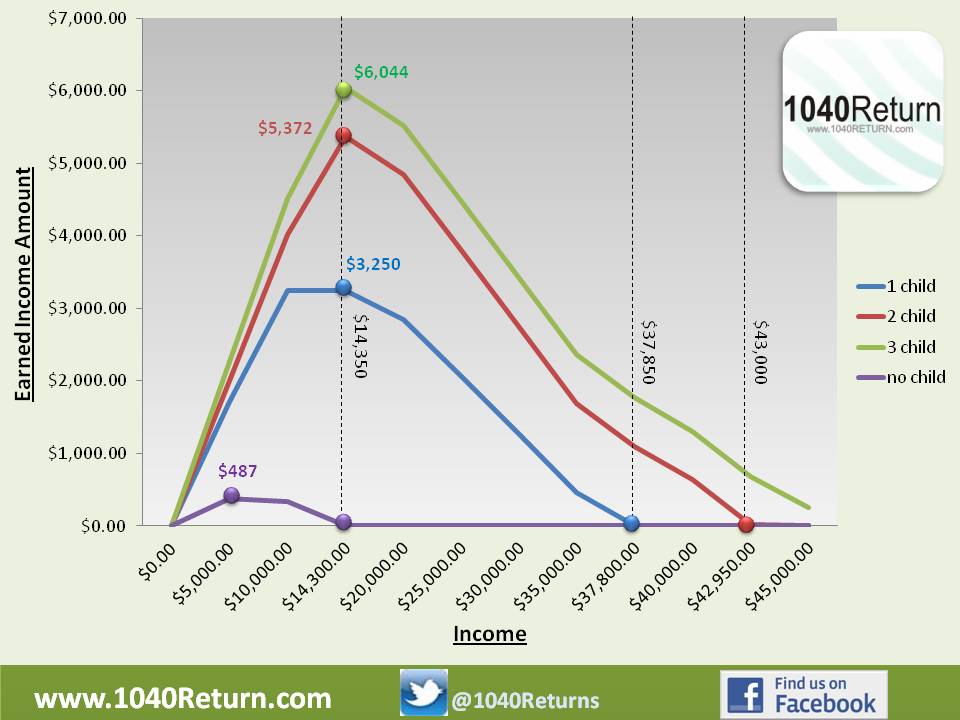

Earned Income Tax Credit 2013 “EIC” is one of the most popular tax credits if you have children. So, what is earned income credit? The government will actually give you money for supporting your children. For example if you have 3 children and filing as Head of Household and earned $14,300.00 last year the government will give you an additional $6,044! Like all tax laws there are certain requirements. So, here are the earned income credit guidelines.

As you can see in the above chart the maximum credit peaks when you earn $14,300.00 per year and the credit starts to phase out as you make more money. To qualify you have to meet the following test. Of course, with all test there are exception to the rule.

1. Relationship test – in another words the dependent must be related by blood such as son, daughter, stepson, stepdaughter, brother, sister, eligible foster child and/or adopted child.

2. Age Test – The child must be under age 19 at the end of 2013 (and younger than the taxpayer), or under age 24 at the end of 2013 and a full-time student during any part of any 5 months during 2013, or any age if permanently and total disabled.

3. Your child must have lived with you in the United States for more than half of 2013 and have a social security number. This means the 50 states and the District of Columbia. It does not include Puerto Rico or U.S. possessions such as Guam.

4. All filing status qualifies for the Earned Income Tax Credit except married filing separately.

5. You must be a U.S. citizen or resident alien all year. Children that are born in 2013 are considered living all year for tax purpose. For example if a child was born on December 31st. The child qualifies for the earned income tax credit 2013.

6. The income must be earned – Examples of earned income are wages, salaries, tips, and other taxable employee compensation. Also this includes net earnings from self-employment.

7. Finally, if the tax payer has investment income of more than $3,300.00 (for 2013), he or she may not claim the EIC. For example: taxable interest, tax exempt interest, dividend income, capital gain net income, certain income from rents or royalties, and certain income from passive activities.

Login now to 1040Return